ACA Premiums Surge in 2027: Wallet Warning & Survival Tips

Health insurance costs under the Affordable Care Act (ACA) are poised for another significant increase in 2027. With premiums expected to climb 5-12% on average nationwide, millions of Americans face higher monthly bills just as open enrollment approaches. This jump comes amid rising medical costs, insurer adjustments, and lingering effects from recent policy shifts. If you’re one of the 21 million people relying on ACA marketplace plans, now is the time to prepare your budget and explore options.

Why Premiums Are Climbing Again

Insurers cite several drivers behind the 2027 hikes. Medical inflation, particularly in hospital and prescription drug costs, tops the list. New treatments for chronic conditions and specialty drugs are pushing expenses higher. Additionally, the end of enhanced federal subsidies from the American Rescue Plan and Inflation Reduction Act means more consumers will shoulder full costs starting in 2026, indirectly influencing rate filings.

State-by-state variations are stark. In high-cost areas like New York and California, increases could exceed 15%, while rural markets in the Midwest may see more moderate 4-7% bumps. Factors like the number of competing insurers and local healthcare utilization rates play major roles. Early filings from major carriers such as UnitedHealthcare and Blue Cross Blue Shield indicate these trends will hold through 2027.

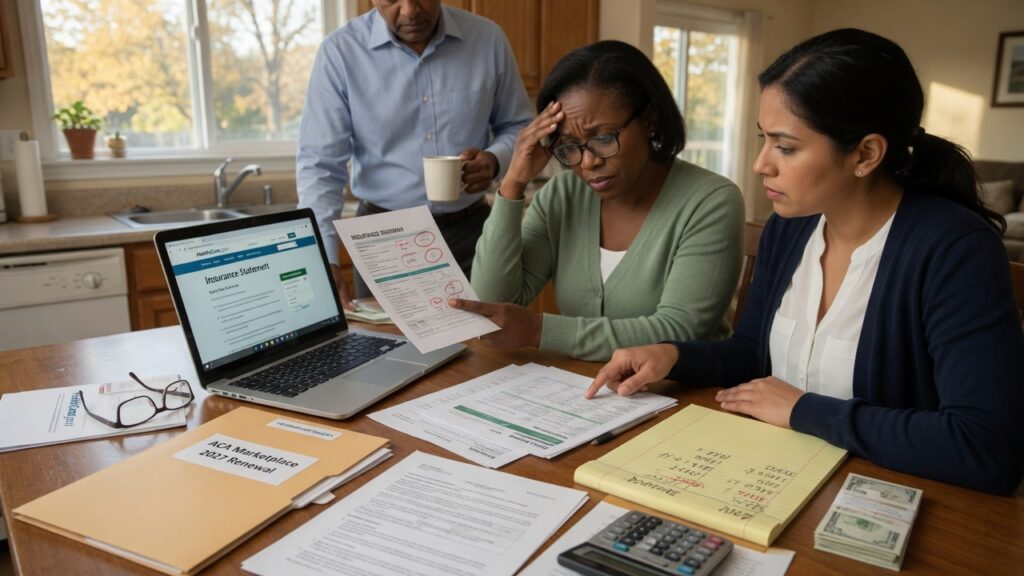

Impact on Your Wallet

For a typical family of four earning around $80,000 annually, this could translate to an extra $150-300 per month without subsidies. Bronze plans, often the most affordable entry point, are seeing the steepest relative increases. Even silver plans with cost-sharing reductions may not fully offset the pain for middle-income households.

Young adults and self-employed workers are particularly vulnerable. Those just above subsidy eligibility thresholds (400% of the federal poverty level) will feel the brunt. Retirees not yet on Medicare and gig economy participants should brace for sticker shock during November’s open enrollment period.

How to Shield Yourself from Higher Costs

Proactive steps can mitigate the damage:

- Shop during open enrollment: Compare plans on Healthcare.gov or your state exchange between November 1 and January 15. Use the preview tools to model 2027 rates early.

- Maximize subsidies: Verify your income projection accurately. Changes in household size or job status could qualify you for premium tax credits.

- Consider plan tiers wisely: A gold plan might offer better value if you anticipate high usage, despite higher premiums.

- Explore alternatives: Health-sharing ministries or short-term plans (where legal) may provide temporary relief, though they lack ACA protections.

Tech tools are making this easier than ever. Apps like eHealth and Stride integrate with ACA data to provide personalized comparisons, including projected out-of-pocket maximums.

Looking Ahead to 2027 and Beyond

Policymakers are debating extensions of enhanced subsidies, which could blunt some increases if passed. Meanwhile, insurers are experimenting with telehealth mandates and value-based care contracts to control long-term costs. Consumers should monitor CMS announcements for any mid-year adjustments.

Staying informed is your best defense. Bookmark reliable sources like the Kaiser Family Foundation for rate trackers and set calendar reminders for enrollment deadlines. With strategic planning, you can navigate the 2027 premium surge without derailing your finances.

The ACA marketplace has weathered previous storms, but individual vigilance remains key. Review your current coverage today and prepare for what’s ahead—your wallet will thank you.